1. The Financial Supervisory Agency ("the Agency") acknowledges that the non-performing assets problem in our country is deeply rooted in the lack of confidence in the financial condition of financial institutions as well as its public disclosure. Under the circumstances, the Agency has already undertaken a series of actions to remedy the situation fundamentally in conformity with a principle to pursue transparent and fair financial supervision based on clear rules. Specifically, we have issued an order for financial institutions to report the results of their self-assessment of asset quality according to relevant laws and regulations. Following the reports, we will conduct intensive urgent inspection, in collaboration with the Bank of Japan, of the 19 major banks. Based upon the results of the inspection, we will take, if necessary, strict remedial measures as required by the Prompt Corrective Action. The Agency believes that to respect fully this sort of definitive move, from the old oversight of the so-called "convoy system" to ex post facto checking oversight based on clear rules, will be an essential part to revitalize the financial system through securing confidence at home and abroad in the soundness of financial insitutions in Japan as well as inducing financial institutions to fully abide by market disciplines.

2. On the basis of the basic perspectives as mentioned above, the Agency believes that the following steps, including disposal of bad loans, should be taken for the financial revitalization. Public disclosure based on standards comparable to those set by the Securities and Exchange Commission (SEC) in the United States, and enforcement of market disciplines among financial institutions by the supervision of the Agency, together with various measures set out in the Comprehensive Plan to Enhance the Liquidity of Real Estate and Bank Loan Assets published on April 23, 1998, will facilitate the removal of bad loans from the balance sheet. In parallel with this, the reorganization of financial institutions is expected to advance through market mechanism. The Agency will make its utmost effort to stabilize the financial system utilizing, if necessary, the framework of public funds backed by the Two Acts for Financial Stabilization, and to minimize social and economic cost incurred by the failure of financial institutions through the utilization of the Bridge Bank system to be introduced.

3. On the other hand, securing confidence at home and abroad in

financial supervision is integral to the rejuvenation of the financial

system. While the Agency intends to take all possible measures

to fulfill its duties, it is essential to strengthen and reinforce

the organizational structure of the Agency. The Agency will immediately

start discussion towards realizing a new system for more effective

inspection, off-sight monitoring and supervision, as set out in

the Second Report of the Comprehensive Plan for Financial Revitalization

published today. For this purpose, we will make public an inspection

manual and carry out continuous off-sight monitoring of financial

institutions. Furthermore, we plan to introduce a new method aiming

to improve the quality of inspection by taking advantage of external

expertise, and to expand the personnel base of the Agency. Through

these efforts, we will establish an administrative organization

necessary for reconstructing the financial system.

[ Provisional Translation ]

July 2, 1998

Government-Ruling Party Conference

to Promote the Comprehensive Plan

for Financial Revitalization

I INTRODUCTION

It is of highest priority and urgency for the Government of Japan to address the non-performing assets problem. We must grapple with the problem in a comprehensive manner, while quickly implementing necessary measures starting with those that are feasible.

From this viewpoint, the Government-Ruling Party Conference, announced on June 23 measures centering around the liquidation of land and loan assets and the promotion of effective utilization of land in the first report on the Comprehensive Plan for Financial Revitalization. We expect financial institutions to aggressively promote, hereafter, the disposal of bad loans by taking advantage of the conducive environment created by such measures. On the other hand, it is also very critical for the reconstruction of our economy to ensure the stability of the financial system and its restructuring by having financial institutions and others concentrate on the fundamental settlement of bad loans, thus securing confidence both at home and abroad.

Based on these considerations, the Conference has drafted the following measures.

These initiatives represent a system and mechanism that are both comprehensive and detailed, constructed around such pillars as (a) aggressive disposal of bad loans, (b) prompt restructuring of financial institutions, (c) improvement of transparency and disclosure, and (d) strengthening of bank supervision and prudential standards, to work toward the resolution of the non-performing loan problem.

We will make every effort to implement the

measures as soon as possible, including, in particular, promptly

submitting the necessary bills to the Diet.

II SPECIFIC MEASURES

1. Creating Systematic Framework to Promote

Aggressive Disposal of Bad Loans

(1) Establishing Secondary Market for

Bad Loans, etc.

To facilitate the marketing of bad loans by banks, it is critical to establish a secondary market with depth through the use of such methods as bulk sales and securitization. Aiming at promptly creating such a market, we will:

(Note) Maximum hypothec is one

type of hypothec, which secures a series of both existing and

future credits within the contracted amount so that the amount

covered by the lien changes from time to time.

(2) Enhancing Infrastructure to Facilitate

Disposal of Bad Loans

The Law on Securitization of Specified Assets

by Special Purpose Companies (or SPC Law) was approved by the

Diet in the previous session to serve as a legal infrastructure

to facilitate the disposal of bad loans by financial institutions

through securitization. In preparation for its implementation

on September 1 this year, we will continue to make the necessary

preparations, such as working out the details of the Plans on

Securitization of Assets. At the same time, we will promote the

improvement of infrastructure for the disposal of bad loans by

taking such actions as submitting to the next Diet Session bills

to establish the Temporary Council for Coordinating Real Estate-Related

Rights (tentative name).

2. Improving Transparency and Disclosure

To secure confidence both at home and abroad in Japan's financial institutions, a standard equivalent to the SEC standard has been adopted for the disclosure of bad loans since the accounting year ending March this year. Furthermore, the Financial System Reform Law, enacted in the last Diet Session, mandates, through sanctions, that all financial institutions disclose, following the standard equivalent to the SEC standard, their financial information on a consolidated basis starting from the accounting period ending March next year. Furthermore, as part of the initiative to adopt international standards on accounting and disclosure, we will aim to introduce mark-to-market accounting for financial instruments from March 2001.

In line with such developments, financial

institutions and others will increasingly need to make their management

styles more responsive to the market. Thus, financial institutions

and others are expected to promote voluntary and aggressive disclosure

to attract investors in the market.

3. Strengthening Bank Supervision and Prudential

Standards

(1) Creation of a Financial Supervisory

Agency

The Financial Supervisory Agency (FSA) was

created on June 22 as a body to perform transparent and fair financial

supervision based on clear rules, ensuring the move from oversight

based on ex ante discretionary guidance to ex post facto checking

oversight based on laws and regulations.

(2) Intensive Inspection of Major Banks

In accordance with Article 24 of the Bank

Act, the FSA has already issued an order requiring financial institutions

to report the results of their self-assessment of asset quality.

Following these reports, the FSA will immediately carry out an

intensive inspection of 19 major banks, in collaboration with

the Bank of Japan, and further examine the current situation at

these institutions.

(3) Strict Measures based on Prompt

Corrective Action

Based on the results of the inspection, strict

measures will be taken, if necessary, according to capital-adequacy-ratio

classifications, including the use of Prompt Corrective Action

ranging from implementation of management improvement plans to

suspension of operations.

(4) Strengthening of Organizational

Structure for Inspection, Surveillance, and Supervision

Inspection manuals and checklists incorporating external expertise will be adopted for government inspections, and made public by the end of this year. Also, follow-up on the improvements made after the inspection and monitoring, including continued analysis of financial statements, will be conducted, with the aid of a computer system to be set up for this purpose.

To strengthen and reinforce inspections in a wider sense, we will ensure that government inspections, internal inspections by financial institutions, and external auditing by certified public accountants are efficiently coordinated. We will also promptly decide upon a new mechanism for third-party operation of government inspections and introduction of private-sector expertise.

Regarding the inspection, surveillance and

supervision functions of the FSA, we will systematically improve

the organization, including substantial expansion, through a prompt

review taking into account the organizational structure of financial

inspection and supervisory authorities in other countries.

4. Stabilizing and Strengthening the Functions

of the Financial System

While the administration will be transformed

into one based on rules founded on market principles and the principle

of self-responsibility, there may be cases where some financial

institutions fall into trouble during the process of aggressively

disposing of bad loans. Should such cases arise, it would be necessary

to ensure the protection of depositors and the stabilization of

the financial system, while at the same time taking appropriate

measures for good-faith and sound borrowers.

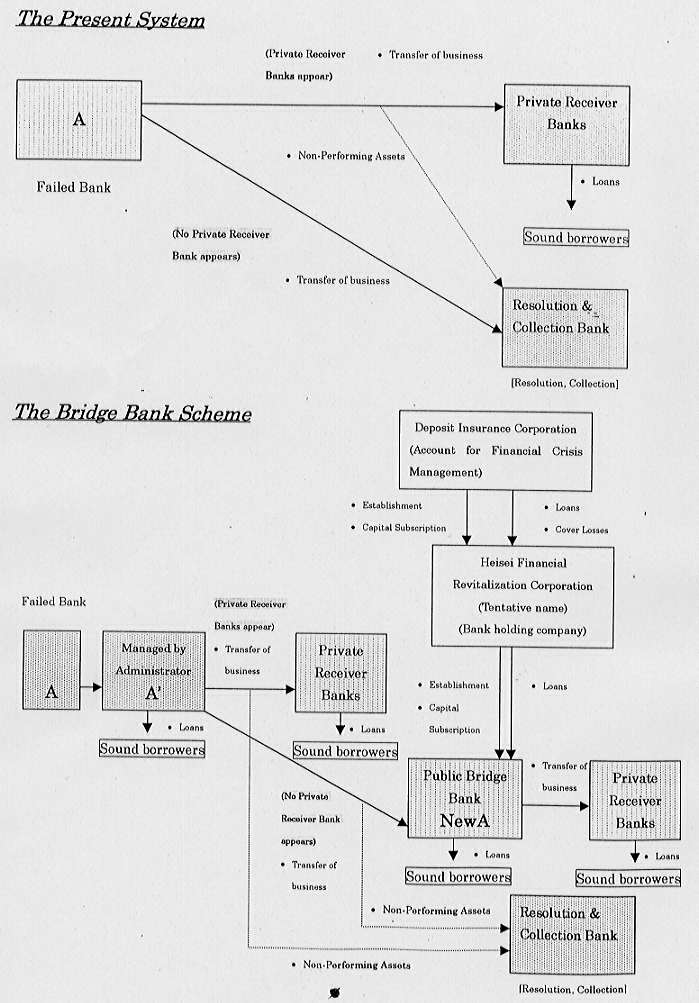

(1) The Introduction of Bridge Bank

a. Basic perspectives

(i) In order to ensure the stability of the

financial system and protection of depositors, it is important

to strengthen the framework to deal with failure of banks promptly

and effectively, particularly by expanding the existing scheme

to cover those cases where no private receiver bank exists to

assume operations of the failed banks, thereby restoring the confidence

in the financial system as soon as possible.

(ii) It is also necessary to prepare a framework

that contributes to providing appropriate measures for dealing

with sound borrowers in good faith who cannot find new lenders

in such a case.

(iii) For this purpose, an institutional

scheme will be introduced for publicly administering the business

of failed banks promptly after the failure of the banks. In addition,

an institutional framework will be introduced that enables establishment

of new public banks as bridge banks to maintain loans to sound

borrowers in good faith even if no private receiver bank appears.

In this case, the fundamental objectives should be to stabilize

the financial system and to protect depositors by smoother resolution

of failed banks through this framework, and from such standpoints,

the Deposit Insurance Corporation (DIC) will be utilized.

(iv) A checking system for strict examination

of borrowers and loans will also be established.

b. Concrete aspects of the scheme

The scheme is consisted of the following

two stages and taken together, the scheme will be virtually equivalent

to the bridge bank scheme in the U.S.

(i) Business management of failed banks by financial administrators (receivers)

(Note) Measures should be put in place for recruiting persons qualified to be financial administrators.

From this standpoint, a legal framework for ensuring smooth transfer of the business of failed banks will be put in place (such as special provisions in case a shareholders meeting to decide the transfer of the business cannot be convened, and those for facilitating transfers of fixed mortgage (maximum hypothec)).

(ii) Establishment of public bridge banks

(Note) The DIC will utilize \13 trillion public funds secured for stabilizing the financial system (earmarked for financial crisis management).

(Note) The bridge banks will not only receive public funds but also be available for capital subscription by the private sector.

(Note) Funds for mitigating the credit crunch appropriated in the fiscal 1998 budget will be utilized.

(iii) It is necessary to make effort to maintain

transparency in establishing and operating this scheme.

(iv) In order to establish this institutional

framework, necessary bills will be brought in the next Diet.

(2) Utilizing the 13 Trillion Yen Fund

of Government Financial Institutions to Cope with the Credit Crunch

Governmental financial institutions have

secured an appropriation amounting to about 13 trillion yen for

FY 1998, in order to cope with the credit crunch, and will continue

to actively and properly handle the credit demands of small and

medium-sized enterprises, middle-ranked corporation, and others.

(3) Merger, Acquisition, and Resolution,

and Restructuring of Financial Institutions through Utilization

of 30 Trillion Yen Secured by Two Laws for Financial Stabilization

In the course of the merger, acquisition and, resolution of the financial institutions, the stability of the financial system and the protection of depositors are indispensable. More specifically, thorough protection of depositors will be sought by utilizing the 17 trillion yen appropriated under two laws for financial stabilization, and restructuring of the financial institutions will be sought through timely and appropriate resolution of failed banks.

Furthermore, it is critical also that private

financial institutions aggressively engage in resolution and restructuring.

Therefore, complete implementation of the Plan for Ensuring Sound

Management, including the appropriate disposal of assets, such

as write-offs, allowance of reserves, and sales as well as restructuring,

will be necessary to utilize the 13 trillion yen in public funds.

We strongly expect that merger, acquisition, and resolution of

the financial institutions and restructuring of the financial

system will be accomplished through these measures.

(4) Preventing

the Bailing out of Managers and Shareholders of Failed Banks

When resolving failed banks, it will be ensured

that the managers are not bailed out but resign and are subject

to prosecution in accordance with civil and criminal codes, and

that the shareholders suffer the loss.

III. SUMMARY

In preparation for the substantial reform of the financial system, Japanese financial institutions have to promptly dispose of their bad loans. The measures set out above, together with the concepts described in our first report on the comprehensive plan, present overall measures for the revitalization of the Japanese financial system.

We expect that the measures set out above

will bring about the vitalization of the financial system and,

further, the prompt recovery of the economy.