|

|

| Greeting by Minister for Financial Services Shozaburo Jimi (center) at Meeting of Directors-General of Local Finance Bureaus (November 1) |

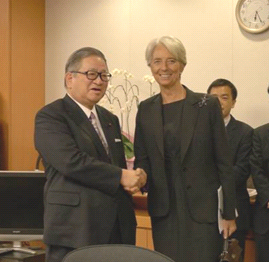

IMF Managing Director Christine Lagarde (left) shakes hands with Minister for Financial Services Shozaburo Jimi (right) (at Minister's Office) (November 11) |

[Photo Gallery]

Meeting with IMF Managing Director Christine Lagarde

* Minister for Financial Services Shozaburo Jimi met with IMF Managing Director Christine Lagarde at the FSA Minister's Office on November 11.

|

|

Meeting of Directors-General of Local Finance Bureaus

* Greetings by Senior Vice Minister Ikko Nakatsuka (lower left photo) and Parliamentary Secretary Hiroshi Ogushi (lower right photo), at the Meeting of Directors-General of Local Finance Bureaus (upper photo) held on November 1.

|

|

[Topics]

Revision Again of Current Action Plan on Fostering People who Passed the CPA Exam and Expanding their Fields of Activity

1. Situation of Initiatives until Now

-

(1) With the aim of having people who passed the CPA exam work in a wide variety of fields in the society and economy, opinion sharing meetings have been held since April 2009 by the FSA, Certified Public Accountants and Auditing Oversight Board, Japanese Institute of Certified Public Accountants, Keidanren, and four financial organizations. In July 2009, a midterm report and current action plan were put together regarding response policies needed to resolve issues. Moreover, an opinion sharing meeting was held in November 2010, the action plan was revised, and new policies were added.

-

(2) Thereafter, as a result of initiatives advanced by each member, one may think that there is a certain degree of progress in expanding their fields of activities, but one cannot say we have reached the point where people who passed the CPA exam are widely used in society and economy. Therefore, from the viewpoint that related parties need to investigate in more depth, opinion sharing meetings are being held since August 2011 to proceed with investigations on whether there are further feasible response policies, unconstrained by the framework until now.

-

(3) In November 2011, policies discussed in opinion sharing meetings were summarized, the current action plan was revised again, and each member agreed to actively work in accordance with the action plan after it was revised again.

2. Main Points of Current Action Plan (Revised Again)

-

(1) Development of Framework for Assistance in Audit Work by Fixed Term Employment in Small and Medium Audit Firms

- Develop a framework for small and medium audit firms to employ for a fixed term people who passed the CPA exam, or sign outsourcing contracts with them, and have them assist in audit work

-

(2) Calls for the Business World to Hire More People Who Passed the CPA Exam

- Obtain the cooperation of business organizations and securities exchanges, and distribute PR leaflets and post notices on the home pages of EDINET and various organizations, to inform the business world that people can obtain the qualification even if they work on financial analysis in term employment or consulting companies, etc. Also call on them to hire more people who passed the CPA exam

- Obtain the cooperation of securities exchanges, send questionnaires to enterprises, and learn the actual situation of hiring people who passed the CPA exam

-

(3) Expansion of Work which Qualifies as Practical Employment

- The practical employment requirement for obtaining the CPA qualification is expanded to include clerical work on financial analysis such as cost calculations and settlement document preparations done in disclosure companies and in consolidated subsidiaries (including overseas subsidiaries) of disclosure companies and of corporations with at least 500 million yen of capital (investment received), and expanded to include practical work (financial analysis) other than inspections in national and local public bodies

- This clarifies that forms of employment engaged in practical work are not excluded, even if not regular employees

* For details, please go to the FSA's web site and access “Opinion Sharing Meeting and Revision Again of Current Action Plan on Fostering People who Passed the CPA Exam and Expanding their Fields of Activity” (November 2) at the Press Releases section. (Available in Japanese only)

Results of the public comments on the Draft Government Ordinance and Cabinet Office Ordinance, etc. on the 2011 revision of the Financial Instruments and Exchange Act (Enforced within Six Months)

The FSA published the Draft Government Ordinance and Cabinet Office Ordinances, etc. on the 2011 revision of the Financial Instruments and Exchange Act (Enforced within Six Months), and widely solicited public opinions from August 30 to September 30. The results, etc. were published on November 11, 2011.

The cabinet order was decided by cabinet resolution on November 11, 2011, and was promulgated on November 16, 2011, together with a related cabinet office ordinance. The cabinet order and cabinet office ordinance will come into force on November 24, 2011.

An outline of this cabinet order and cabinet office ordinance is as follows.

1. Change to notification system for representing the businesses or carrying out services on behalf of other insurance companies within insurance group companies

The scope of an insurance group company is stipulated to be subsidiary companies, a major shareholder who holds over 50% of voting rights, fellow subsidiaries and so on of that company.

2. More flexible regulations on asset securitization schemes

-

(1) To simplify procedures for changing an asset securitization plan, this stipulates what are “minor changes” of an asset securitization plan which do not require notification.

-

(2) To relax regulations on asset acquisition, this stipulates what are “Accessory Specified Assets” which do not require the obligation to set up a trust, etc. when acquiring assets.

-

(3) To simplify fundraising procedures, the requirements for bridge financing (borrowings other than specific borrowings) are relaxed.

3. Response to trading of unlisted shares by unregistered business operators

The order stipulated that the securities subject to the transaction invalidation rule are corporate bonds, stocks, share options, etc.

* For details, please refer to “Results of the Public Comments on the Draft Government Ordinance and Cabinet Office Ordinance etc. on the 2011 revision of the Financial Instruments and Exchange Act (Enforced within Six Months).” (November 11, 2011) in the “Press Releases ”of the FSA website. (Available in Japanese only)

Draft Partial Revision of Public Notices on Capital Adequacy Ratios of Financial Instruments Business Operators, etc. - Results of Public Comments, etc.

The FSA widely solicited opinions on the “Draft Partial Revisions of Public Notices on Capital Adequacy Ratios of Financial Instruments Business Operators, etc.” from July 5 to August 5, 2011. It published the results of public comments on November 22, 2011, and partially revised public notices, etc.

Below is an outline of the revisions.

1. Background of Partial Revisions of “Public Notices on Capital Adequacy Ratios of Financial Instruments Business Operators, etc.”

-

(1) With the revision of Financial Instruments and Exchange Act in 2010, group basis supervisory regulations for securities companies (consolidated capital adequacy ratios, etc.) were introduced in April 2011. Three capital regulations are now imposed on securities companies: non-consolidated, downstream consolidated and upstream consolidated.

-

(2) The “Final Package of Measures to Enhance Three Pillars of Basel II” (called “Basel 2.5”) was announced in July 2009. This was mainly an agreement on enhanced treatment of securitized products and market risks. Given that its international implementation is sought by this December, upstream consolidated regulations were revised this May 27 (this revision was similar to the public notice on bank's consolidated capital adequacy regulations).

-

(3) Regarding public notices of non-consolidated and downstream consolidated regulations, calculation of market risks which are a major factor has basically been using the same calculation method as in Basel II, with consideration of the securities company's business model, while giving conservative treatment to low liquidity assets.

-

(4) This time, market risk related sections in public notices on non-consolidated and downstream regulations were also revised, similar to revisions of public notices on upstream consolidated regulations.

2. Main Contents

-

(1) Raise the risk weights of securitized products and re-securitized products

-

(2) Introduce monitoring requirements concerning external ratings use

-

(3) Capture trading account related stress VaR, additional risks (credit risks), etc.

-

(4) Introduce expected exposure method

-

(5) Others (Clarification of scope of government bonds. Consistency with public notices of upstream consolidated regulations regarding requirements of internal control model method)

3. Implementation Dates

This revised public notice shall apply starting on March 31, 2012 (however, financial instruments business operators which are subsidiaries of bank holding companies, banks, designated parent companies, etc. can choose to apply it starting on December 31, 2011).

* For details, please go to the FSA's web site and access “Draft Partial Revisions of Public Notices on Capital Adequacy Ratios of Financial Instruments Business Operators, etc. - Results of public comments, etc.” (November 22) at the Press Releases section. (Available in Japanese only)

Site Map

- Press Releases & Public Relations

- Press Releases

- Press Conferences

- Official Statements

- FSA Weekly Review & ACCESS FSA

- Speeches

- For Financial Users

- Others

- Archives

- Laws & Regulations

- Name of Laws and Regulations(PDF)

- Recent Changes (Legislation, Ordinances, Guidelines)

- Guidelines

- Financial Instruments and Exchange Act

- Financial Monitoring Policy

- Public Comment

- No-Action Letter System

- Procedures concerning Foreign Account Management Institutions