Greeting by Senior Vice-Minister of Shozo Azuma |

Greeting by Minister Shozaburo Jimi at Meeting |

[Photo Gallery]

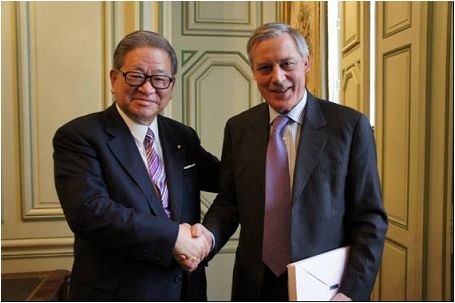

Minister Shozaburo Jimi visited France and Belgium on a five day schedule starting January 9. In France, he held meetings with Christine Lagarde (Minister of Economic Affairs, Finances and Industry, 1st photo below), Christian Noyer (Governor of the Banque De France, 2nd photo below), Eric Besson (Minister of Industry, Energy and the Digital economy under the Minister of Economy, Finance and Industry), and Jean-Paul Bailly (President of La Poste Group).

In Belgium, he held a meeting with European Commissioner Michel Barnier.

|

| Christine Lagarde, French Minister of Economic Affairs, Finances and Industry (left) shakes hands with Minister Shozaburo Jimi |

|

| Christian Noyer, Governor of the Banque De France shakes hands with Minister Shozaburo Jimi |

[Featured]

International Conference on The Role of the Financial Sector in Promoting Economic Growth in Asia (February 3, 2011)

The Financial Research Center of the Financial Services Agency (FSA Institute) hosts joint international conferences which bring together the financial industry, academia, and the government sector from Asia, Europe and the United States to discuss practical issues concerning the financial system. This year's international conference was jointly hosted by the FSA Institute, the Asian Development Bank Institute (ADBI) and the Keio University Global Center of Excellence (GCOE) Program on February 3, 2011, and was titled “The Role of the Financial Sector in Promoting Economic Growth in Asia.” The conference was attended by over 300 participants from Japan and abroad, including academics, government and central bank officials, financial institutions, and officials from foreign embassies in Tokyo.

At the start of the conference, Shozo Azuma, Senior Vice Minister of Cabinet Office for Financial Services, gave welcoming remarks. The minister stated that, “we aim for our financial markets to grow with Asia through their role as Asia's financial center by deepening and strengthening their functions further. This conference is such a worthwhile opportunity, with participation by researchers, supervisors, and financial institutions from many Asian countries and Australia.”

The conference examined what role the financial sector should play to secure continuous growth in the Asian region and how best financial supervision and regulation could enhance such a role. It also looked at the impact of the global financial crisis on the Asian financial system and implications of the undergoing discussions on global regulatory reforms for Asia.

Following is the summary of the conference prepared by Prof. Naoyuki Yoshino, Director of the FSA Institute and Professor of Economics at Keio University.

Session I: The Development of the Asian Financial and Capital Markets and Its Implications for Financial Regulations

In session I, the impact of the global financial crisis on the financial system was examined and the progress in undergoing discussions on financial regulatory reforms was reported.

Mr. Masamichi Kono (Vice Commissioner for International Affairs, FSA Japan) explained how the recent global financial crisis emerged and how it spread to European and U.S. financial institutions. In response to the emergence of the crisis, bank rescue plans and regulatory responses were taken to stabilize the financial system. By spring 2008 the crisis seemed to have been managed, but in 2010 it turned into sovereign risk issues. Standard-setting bodies such as the Financial Stability Board (FSB) are developing rules and standards in response to the crisis. Mr. Kono stated that there are still some gaps to be addressed, such as the shadow-banking issue. Regarding the FSB and other standard-setting bodies, there should be strong legitimate criticism about their arrangements, governance and transparency given the importance and influence of the rules they set. Rules set by the G20 and the FSB are applied globally so there must be wide support and understanding for their activities. It was pointed out that the situation of Asia is different from the United States and Europe, and therefore Asia's voice must be institutionalized in the process of designing the new regulatory framework.

Mr. Hunsuk Rhee (Deputy Director General, International Cooperation, Financial Services Commission, Republic of Korea) presented Korea's experience in addressing the global financial crisis. At first, Korea was hit by the shortage in foreign currency liquidity, which later turned into credit risk. To cope with the liquidity shortage, the government provided payment guarantee to foreign currency borrowings by Korean banks, and with other measures in place Korea exited from the crisis quickly. He added that one country's efforts are not enough to address risk, and emphasized that coordinated efforts are necessary. He expressed his view that there are pros and cons to universal implementation, but to avoid regulatory arbitrage, rules should be implemented in the same manner across all countries.

Dr. Shogo Ishii (Director, Regional Office for Asia and the Pacific, IMF) described the current global situation as a dichotomy. The global economy is recovering, but the financial system is still unstable. Sovereign risk and banking-sector credit risk are intertwined. The creditworthiness of banks declined as shown in an increase in the credit default swap (CDS) spreads. Recently, as sovereign risk has been increasing, countries' CDS spreads are also increasing.

So far credit growth has remained moderate in general in the Asian region, but asset price pressures are strengthening as seen in the rising trend in the property market in China. Asset reallocation by global investors could increase further capital flows, risking macroeconomic and financial stability. Capital inflows to Asia are likely to continue, and hence a challenge for Asia would be how to manage volatile liquidity to maintain stability in the economy and the financial system.

Mr. Pietro Ginefra (Chief Representative for Japan, Korea and South East Asia, Bank of Italy) commented on recent developments in Europe following the global financial crisis. The global financial crisis revealed a lack of adequate macro-prudential supervision and an absence of truly harmonized rules in Europe. Given the situation, Europe decided to establish the European Systemic Risk Board (ESRB), which is responsible for macro-prudential analysis in Europe, and the European System of Financial Supervisors (ESFS), which is responsible for micro-prudential supervision with national authority and cross-border colleges of supervisors. Since Europe has faced sovereign risk, he pointed out the need for double-checking the effects of bank bailouts on public debt stability. Bank bailouts are useful to stabilize financial markets in the beginning, but later they can cause sovereign risk issues through increased public debt, and therefore decisions on bailouts need to be made carefully.

Session II: The Current State of the Financial Sector and the Regulatory Framework in Asian Economies

Session II looked at the financial systems of China, India, Thailand and the Philippines closely. Presenters from each country explained the current situation and how their financial system dealt with the global financial crisis. The effects of global regulatory reforms, such as Basel III, on their financial systems were also explained.

Mr. Luo Ping (Director General of Training Department, China Banking Regulatory Commission) explained recent developments in China's financial sector.

The key issue for China is how to keep focused on the domestic policy agenda while adopting new global standards. Basel III is another important milestone for capital regulation. However, Basel III is only part of an effective regulatory framework. While phasing in Basel III, China also needs to implement the idea of forward-looking provisioning policy, particularly to address the deterioration of credit quality following huge credit expansion in order to arrest the downturn of the economic activities indirectly affected by the financial crisis. In addition, activity restriction will be another effective tool to prevent banks from getting too complex for bankers to manage and for the regulators to supervise. China will focus on the domestic policy as a priority, while adopting new global standards. Until capital markets in China become mature enough to help finance a significant part of the funding demand, indirect intermediation by banks will continue to be dominant in China's financial situation. Therefore, the challenge remains with respect to how to keep the right balance between enhanced regulation and promoting financial innovation.

Dr. Abhijit Sen Gupta (Associate Professor, Jawaharlal Nehru University, India) presented the impact of the global financial crisis on India's financial system.

Despite a low exposure to the non-performing assets involved in the sub-prime crisis and a gradual approach towards liberalization of the financial sector, certain parts of the Indian financial sector were significantly affected by the global financial crisis. The consequent tightening of the liquidity and the slump in global and domestic demand had a strong adverse effect on the industrial sector, a large part of which is covered by small and medium-sized enterprises (SMEs). Therefore, there was a significant decline in employment and output in some parts of the SME sector. Indian policymakers reacted in a proactive manner, and introduced measures to counter the adverse effect of the financial crisis but the subsequent recovery has not been uniform. With regard to Basel III, the Indian financial sector will be impacted by its introduction. While financial institutions in India are in a comfortable position to meet some of the proposed Basel III standards, the implementation of some of the other standards would be a challenge.

Mr. Bandid Nijathaworn (former Deputy Governor, Bank of Thailand) discussed regulatory reforms carried out in Thailand's financial system.

Financial-sector development in Thailand in the last ten years has been a story of restructuring, adjustment, and renewal. The reform of the regulatory and supervisory framework put in place following the Asian financial crisis was important in rebuilding and strengthening the financial sector, and it brought about a sounder and more resilient financial system. Such strength has enabled the economy to successfully weather the impact of the global financial crisis and helped place the economy on a recovery path. Key to these reforms was the consolidation of the banking sector, initiatives to deepen and broaden the capital market, the reform of the regulatory and supervisory standards under Basel II and IAS 39, and the reform of the legal framework in the financial sector. To further strengthen the financial sector, the reform efforts are continuing under the broad agenda of the Financial Master Plan Phase II, which focuses on improving the financial system's level of efficiency through greater competition, reducing the system cost by addressing the problem of non-performing loans, expanding access to financial services, and strengthening the risk management capacities of banks through complex financial markets and infrastructure in the current global financial crisis.

Mr. Diwa C. Guinigundo (Deputy Governor, Central Bank of the Philippines) presented the financial system of the Philippines.

The Philippine's financial system remained strong after crises in the 1980s and 1990s and even in the recent global financial crisis. Important banking reforms, particularly in the areas of supervision, corporate governance, risk management, and asset clean-up, have strengthened the banking system, boosting its overall performance with higher asset growth, enhanced asset quality, improved profitability and better capitalization. There were also some improvements in other areas of the financial system: the debt market has continued to develop, deposit insurance has been strengthened, and supervisory coordination enhanced. These same reforms served financial institutions well as they were able to stand global financial turbulence. Regulatory authorities are embarking on reforms to further strengthen the financial system with respect to emerging risks and to sharpen macro-prudential tools.

Session III: Challenges for the Asian Financial and Capital Markets and the “Growth Strategy”

In Session III, presenters identified the challenges for Asia's financial markets and provided solutions for such challenges.

Mr. Shigesuke Kashiwagi (Senior Managing Director, Government Affairs and Risk Advisory Group, Nomura Holdings, Inc.) emphasized the importance of fostering Asia's capital markets for further economic growth.

The Asian economy has grown significantly in the last decade. Despite the rapid growth in capital markets, indirect financing accounts for a substantial part of corporate financing, especially in countries such as China, India, and Malaysia. There will be a significant reduction in banks' lending capacity in Asia due to implementation of Basel III rules. Hence, capital markets will increasingly become important for financing in Asia. To this end, the governments of Asian economies are planning to develop capital markets in Asia through regional cooperation, including the Asian Bond Markets Initiative (ABMI). In addition, for further progress, Asia should make financial services into an “industry”; it should create a pan-Asian financial services industry.

Mr. Kashiwagi presented six solutions for achieving further development of Asia's financial system and markets. First, regulators should cooperate for harmonization and standardization of national rules. Second, standardization of hard infrastructure will contribute to more efficient market transactions. Third, regulators should engage in global regulatory reform discussions and carefully consider possible impacts that the new regulations, such as liquidity rules, would have on the region's capital market activities as they would raise the cost of market making. Fourth, development of reliable and efficient settlement systems will increase the resilience of the financial markets. Settlement systems are one of the most important infrastructures, especially for growing economies which need smooth money flows and market activities. Fifth, each country, city, or region should seek a core competitive skill set to make a pan-Asian financial services industry. And sixth, a consistent and predictable regulatory/supervisory approach is a crucial element for the private sector in making investment decisions and committing their resources.

Mr. Chikahisa Sumi (Deputy Commissioner for International Affairs and Competitiveness, FSA) presented Japan's growth strategy for financial markets and financial industry. Mr. Sumi briefly explained “The Action Plan for the New Growth Strategy,” published by the FSA in December 2010, which summarizes necessary measures for the financial sector to promote economic growth. The action plan placed a focus on the importance of the growing Asia.

Mr. Sumi then described the situation of the Japanese financial system. Subprime loan products had limited direct impact on the Japanese financial sector, partly because Japanese financial institutions had implemented Basel II before the crisis. According to Basel II, unrated securitization exposures are deducted from capital unless a bank can appropriately capture the risk profile of their underlying assets. Therefore, banks were reluctant to purchase subprime products. The small exposure to toxic assets generally limited the losses from these assets for Asian financial institutions.

On the other hand, Japanese financial institutions were damaged by the subprime problem indirectly through contraction of external demand and valuation losses of equity holdings. Therefore, policy measures taken in Japan against the global financial crisis focused on maintaining financial intermediary functions, and were different from measures taken in the United States and Europe. These measures include capital injection to 11 regional financial institutions.

For Asian economic development, Asian countries need to make further investment in infrastructure. To this end, these countries need capital for investment. However, capital flows into Asia are not always stable; capital comes in quickly but can leave quickly. Therefore, these countries need to promote regional cooperation such as Chiang Mai Initiative (CMI) and ABMI in order to attract long-term funds.

Ms. Belinda Gibson (Deputy Chairman, Australian Securities and Investments Commission) emphasized the importance of regulatory cooperation. At international and regional levels, cooperation and coordination are critical to reduce arbitrage risks. Regulators must keep all regulatory provisions within a zone, especially in credit ratings. Information on capital inflows is not transparent to regulators. Information sharing between regulators would be useful.

Mr. Jiro Seguchi (President and Representative Director, Merrill Lynch Japan Securities Co., Ltd., Country Executive for Japan, Co-Head of Asia Pacific Corporate and Investment Banking, Bank of America Group) identified the challenge for Asia and discussed what the banking sector can do to address that challenge.

The challenge for Asia is how to make the current economic growth sustainable. There are two roles on the part of the banking sector in this regard. First, banks in Asia should have in place infrastructure and capacity to utilize excess capital within Asia. Specifically, banks need to implement stringent risk management in order to effectively utilize capital. And second, they should build infrastructure so that stable, long-term capital can be introduced to the region. On the part of regulators, they should work to establish robust and consistent standards across Asia. Consistent rules on governance structure will be crucial for financial institutions in making appropriate decisions in the changing financial situation. Transparency and disclosure are also important for efficient capital markets.

Session IV: Panel Discussion

The chairman of this session, Prof. Yoshino, summarized the discussions made in sessions I, II and III. The financial environment in Asia is different from those in the United States and Europe. For example, SMEs account for a significant part of the economy in Asia, and the financial system is bank-oriented, as bank lending is the most important financing means for many businesses. In some countries, access to credit remains difficult. Such unique features of Asia's financial system need to be taken into account when considering the roles the financial sector plays in promoting economic growth.

Discussions by panelists then took place. The summary of the discussions are as follows.

The situation of Asia's financial system is different from that of the global financial system. Asia's financial structure is dominated by the banking sector and banks are not as efficient and transparent as those in the United States or Europe. Hence, global discussions on regulatory reforms under the G20 and the FSB seem to focus on issues different from what Asia is facing. Asia should promote its voice to be heard in the global discussions.

Promoting access to finance and consumer education is important for continuing economic growth in the Asian region. The lack of financial products and the difficulty SMEs face to receiving credit from banks are issues that need to be dealt with to achieve further economic growth and to enable the fruit of economic growth to be distributed to a wider population. In relation to promoting access to finance, there is an issue that micro credit is not under the supervision of financial regulators or central banks.

Under the globalization of the financial markets, much more progress in the financial sector will be needed to strengthen regulation and supervision in Asia.

* For further details of the conference, please refer to the Conference Materials for International Conference on “The Role of the Financial Sector in Promoting Economic Growth in Asia” on the website of the FSA Institute. The conference program, presentation materials and a summary of the conference can be downloaded from the site.

[Topics]

The 128th & 129th Compulsory Automobile Liability Insurance Councils were held on January 14 and 20, 2011. Discussions were held about results of verification of the standard rates of compulsory automobile liability insurance.

As a result of the discussions, the standard rates of compulsory automobile liability insurance will be raised by 11.7% on average on April 1, 2011.

1. Results of Verification of Compulsory Automobile Liability Insurance Rates

In order to ensure proper standard rates for compulsory automobile liability insurance premiums, the Non-Life Insurance Rating Organization of Japan verifies their propriety each year, and reports the verification results to the FSA Commissioner. The FSA Commissioner reports these verification results to this Council. If the verification results in a decision that the standard rates are improper, then the standard rates are revised.

The loss ratios according to the FY2010 rate verification results reported at the 128th Compulsory Automobile Liability Insurance Council are as follows.

(unit: %)

| Contract year | FY2010 | FY2011 |

|---|---|---|

| Previous (April 2008) planned loss ratio at time of revision |

133.8 | |

| Planned loss ratio according to FY2010 rates investigation results |

139.3 | 139.9 |

UUnder the current standard rates of compulsory automobile liability insurance, assuming that the cumulative balance of revenue and expenditure and cumulative investment profits until the 2007 contract year are to be returned over a five year period, at the rates reduced in April 2008, the planned loss ratio of the net insurance rates is 133.8%. According to FY2010 rate verification result, the 2011 contract year's loss ratio of the net insurance rate is forecast at 139.9%, which exceeds the planned loss ratio. This showed that if the current standard rates are continued, it will be necessary to compensate for the cumulative expenditure which will exceed cumulative revenue in FY2012.

For the future rate level, the opinion was given that “In returning the rate to its original level, it is appropriate to return in two stages.” But another opinion was given that “In order to reduce the burden on automobile users, insurance companies should demonstrate a policy of working to reduce administrative costs.”

The 129th Compulsory Automobile Liability Insurance Council concluded on the direction of “While maintaining the framework of revenue/expenditure balance over the five years until FY2012, which was assumed at the time of the rate change in April 2008, regarding the net insurance rates, for the amount of the clear difference vs. the previous time's expectations according to this fiscal year's verification results, it is appropriate to raise the rate in order to adjust this. In doing so, when changing the rates in order to return to the original rate level in FY2013, it will be possible to ease the sudden increase in insurance premium burdens of policyholders.”

In accordance with this thinking, the recommendation is that the new standard rates notified by the Non-Life Insurance Rating Organization of Japan be applied starting April 1, 2011.

The new standard rates will be, for example, 24,950 yen for a personal use automobile two year contract (2,480 yen above the current standard rate of 22,470 yen). For details, refer to the “(Attachment) Compulsory Automobile Liability Insurance Standard Rates Applied inFY201 (by Insurance Period).”

* For the circumstances of the standard rates revision of April 2008, please go to the FSA web site and access “FSA Newsletter No.63” from the FSA Newsletter section.

Reference: What are “Standard Rates”?

The standard rates are one set of insurance rates, calculated by a non-life insurance rating organization. If an insurance company which is a member of a non-life insurance rating organization follows the procedure for notification of using the standard rates calculated by that non-life insurance rating organization as its own insurance rates, then it is deemed as having obtained approval based on the Insurance Business Act. Currently, the Non-Life Insurance Rating Organization of Japan calculates the standard rates of compulsory automobile liability insurance, which are used by all insurance companies which handle compulsory automobile liability insurance.

2. Inquiry Items

In addition to the above, the secretariat explained that, regarding each mutual aid association which conducts compulsory automobile liability insurance business, for changing part of the items concerning mutual aid premiums in mutual aid rules along with the standard rates notice, each administrative agency with jurisdiction will give its approval and agreement. As a result of discussion, it was found that there is no objection to this inquiry item.

3. Report Items

(1) The report on the implementation situation of the proposed compulsory automobile liability insured medical treatment compensation standard stated that it is currently implemented in 45 prefectures, and that discussions will continue towards its early implementation in the remaining two prefectures (Yamanashi and Okayama).

(2) The General Insurance Association of Japan reported on uses of FY2011 investment profits of private insurance companies. The National Federation of Agricultural Co-operative Associations reported on uses of FY2011 investment profits of JA Mutual. The Ministry of Land, Infrastructure, Transport and Tourism reported on uses of FY2011 investment profits of the Motor Vehicle Safety Special Account.

(3) The Ministry of Land, Infrastructure, Transport and Tourism reported on recent initiatives concerning the compulsory automobile liability insurance system.

* For details, please go to the FSA web site and access “Compulsory Automobile Liability Insurance Council” from the from the Councils section. (Available in Japanese only)

Financial Services Agency Disclosure System Working Group Report

~ Development of Legal System for Rights Offering in Japan ~

The Action Plan put together on December 24 for achieving the New Growth Strategy (June 18, 2010 Cabinet Decision) includes “Development of the Disclosure Rules for Smooth Implementation of ‘Rights Offering’ ” as a policy for “Flexible Supply of Funds, etc.”

In this environment, the Disclosure System Working Group deliberated three times since December 2010 regarding development of a legal system, together with “Expansion of Scope of English-Language Disclosures System” (report published on December 17, 2010) to facilitate use of rights offerings (a capital increase by allotment of share options without contribution) as one possible capital increase technique. This report delivers the results of the study by this Disclosure Working Group.

In rights offering, share options are allotted to all shareholders without contributions. It is one capital increase technique, along with “publicly offering” and “capital increase through third-party allotment.”

A shareholder can exercise his/her allotted share options and pay money, acquiring shares. Meanwhile, instead of exercising these share options, the shareholder can sell them in the market. Therefore, it has the feature that a shareholder who does not want a decrease in his/her shareholding percentage can avoid that by exercising his/her share options, while a shareholder who does not want to invest additional capital can avoid that additional payment by selling his/her share options.

Rights offering is a capital increase technique widely used in Europe, especially for large capital increases. Investors etc. are calling for active use of rights offerings, as it can be a capital increase technique which pays attention to fair treatment of existing shareholders because it could protect the shareholding ratios of existing shareholders.

In order to facilitate use of rights offerings, it is hoped that, based on the proposals of this report which are summarized below, related parties will appropriately advance the development of the legal system.

(1) More Flexible Methods of Delivering Prospectuses

In order to shorten the time and lower the cost regarding rights offering while ensuring investor protection, if the following conditions are met, it is appropriate not to require delivery of prospectuses;

(i) It is rights offering in which the share options are listed on a financial instruments exchange

(ii) Securities registration statement is submitted (resulting in its posting in an electronic disclosure system (EDINET))

(iii) Information such as EDINET's web site address is published in daily newspapers as soon as possible after submission of the securities registration statement (at latest, by the time the share option allotment is made)

(2) Review the Scope of Underwriting of Securities

In rights offerings, there could be a scheme in which share options which are not exercised are acquired by the issuer based on the acquisition conditions, then sold to securities companies, and those securities companies exercise these share options to acquire shares and sell them in the market or to others (referred to hereinafter as “commitment type rights offering”). From a viewpoint of acts of a securities company making a commitment, as the securities company gives a prior promise to acquire and exercise the portion of the issued share options which are not exercised by investors (including existing shareholders), its form of action and risk taking would indicate that there are similarities as if the securities company acts as an underwriter. Therefore, it is appropriate that acts of a securities company which makes a commitment (acquisition and exercise of unexercised share options) are positioned as underwriting of securities, and a framework to impose necessary regulations on securities companies need to be put in place for ensuring investor protection.

(3) Other Issues

It is also appropriate to study handling of regulations on tender offers and on reports of possession of large volume, and correspondence to securities regulations of foreign countries.

* For details, please go to the FSA web site and access “ ‘FSA Disclosure System Working Group Report’~ Development of Legal System for ‘Rights Offering’ ~ ” (January 19) from the Press Releases section. (Available in Japanese only)

1. Introduction

On February 4, 2011, the FSA revised the “Inspection Manual for Insurance Companies” (hereinafter referred to as “Insurance Inspection Manual”), which was issued and published as an Inspection Bureau Director General Notice. The Insurance Inspection Manual was revised several times since its creation in June 2000, but it was completely revised this time, including reorganization of the overall composition.

An outline etc. of the revised Insurance Inspection Manual is explained in this section below.

For convenience, the pre-revision Insurance Inspection Manual is referred to below as the “Old Manual,” and the post-revision Insurance Inspection Manual as the “Revised Manual.”

2. Background of the Insurance Inspection Manual Revision

The Insurance Inspection Manual's composition and content were greatly revised in June 2006. But revision became necessary again in response to changes in the environment surrounding inspection operations and insurance companies.

In particular, in the Old Manual, for cases where business operation problems occur in insurance companies, (1) Items to check individual problem points were mixed up with items to check the system, making it difficult to verify which of the insurance company's functions are problematic, and where the causes of the problems are, (2) There was a lack of check items to verify whether an organizational system is developed for the insurance company itself to proactively work to improve the problem, making it difficult to verify its proactive improvement function.

Also, the so-called “Lehman Shock” created a need to enhance and strengthen items for verifying more advanced risk management responses of insurance companies.

Consequently, investigating revision of the Insurance Inspection Manual was a topic raised in the “Efforts for Better Regulation in Financial Inspections (Action Plan II)” created in May 2009. After a great deal of consideration, the FSA published a draft revision on December 15, 2010, and gathered public opinions. Then on February 4, 2011, based on the opinions received, the Revised Manual was published, and it was issued and published as an Inspection Bureau Director General Notice.

This Notice will apply to inspections executed on April 1, 2011 or later. Items concerning the roles of actuaries regarding the situation of ability to pay insurance payouts will be applied starting March 31, 2012, accompanying enforcement of the laws and ordinances.

3. Common Format

As one of the reasons for this large revision, content written in the Old Manual was also arranged to emulate the composition of the Financial Inspection Manual, in accordance with the common format of each system.

Specifically, in building each management system, the roles and responsibilities of Management are vital. Therefore, it adopts the same format as the Financial Inspection Manual, and except for the “Business Management (Governance)(for Basic Elements),” it is comprised of three parts: “I. Development and Establishment of System by Management,” “II. Development and Establishment of System by Manager,” “III. Specific issues.” It thus clarified the roles and responsibilities which should be played by Management and Manager.

“I.Development and Establishment of System by Management” emphasizes not only Management developing management policies and organizational frameworks and rules, but also the management system as a dynamic process to constantly improve the existing system, and appropriately 1. Develop policies (Plan), 2. Develop rules and organizational framework (Do), 3. Evaluate (Check), 4. Improve (Action). In other words, verification items are arranged from the viewpoint of whether the so-called PDCA cycle functions effectively.

If problem occurrences are found in verification of “II. Development and Establishment of System by Manager” or “III. Specific issues,” then thoroughly verify which part of this PDCA cycle did not function effectively, thereby leading to problems occurring.Especially,if Management is unaware of weak points and problem points that the inspector found through inspections, then do verification including the possibility that the system is not functioning effectively.

4. Content of Each Checklist

The current revision reorganized and rearranged the verification categories, reducing them from 9 items into 8 items.

The “Product Development Management System Inspection Checklist” of the Old Manual was reorganized and rearranged in the Revised Manual, into “Business Management (Governance)(for Basic Elements)” and product development related checklists such as “Insurance Underwriting Risk Management System.”

The following explains the content of each checklist, including major points changed from the Old Manual (except for changes described above).

(1) Checklist for Business Management (Governance)(for Basic Elements)

To verify the business management of an insurance company, this checklist checks whether the following basic elements are appropriately demonstrated, and whether the insurance company's business management is functioning effectively as a whole: 1. System of business management by the board of directors, etc., 2. Internal audit system, 3. System of audits by the corporate auditors, etc., 4. External audit system, 5. System of checking by actuary. In the Old Manual, the “Checklist for Internal Control System” is positioned as common items overall. But in the Revised Manual, the “Checklist for Internal Control System” was reorganized into this checklist, and in accordance with the Financial Inspection Manual, was positioned as categories for verifying parts which are basic elements of business management (governance) of insurance companies.

(2) Checklist for Legal Compliance

This is a checklist to check whether an insurance company has appropriate legal compliance in conducting its business. Its check items are mainly for whether the legal compliance system is functioning effectively for the insurance company's overall business, and whether the systems for handling of legal violations and anti-social forces are functioning effectively.

(3) Checklist for Insurance Sales Management

This is a checklist to check whether there is appropriate management required to ensure compliance with laws and regulations on insurance solicitation, and to achieve proper insurance solicitation. Its check items are mainly for whether the insurance company's insurance solicitation management system is functioning effectively, and whether the systems for insurance solicitation's customer explanations and insurance solicitation outsourcing and management are functioning effectively.

In comparing with the Old Manual, in the Checkpoints at the top of this checklist, “Insurance solicitor belong to a variety of organizations: insurance company sales staff, tied agencies, independent agencies, composite agencies, etc. Therefore, it writes that “It is necessary to be aware that a uniform management system is insufficient, and to develop and establish these systems.” Also, for independent agencies which have multiple connected insurance companies, new check items were added regarding whether the insurance company is checking whether policies are created for customer information management and to prevent improper solicitations for transfers between connected insurance companies.

(4) Checklist for Customer Protection Management

Customer protection management refers to things which should be done from the viewpoints of protection and enhanced convenience of the insurance company's customers. This covers insurance contract management, insurance payout management, customer support management, customer information management, outsourcing management, conflict of interest management, and management of operations which the insurance company deems necessary for customer protection and enhanced convenience. This is a checklist to check whether each of these management systems is functioning effectively.

This revision includes some changes in the checklist such as the addition of check items concerning management of outsourcing.

(5) Checklist for Comprehensive Risk Management

This is a checklist to check whether the risk management process to achieve the insurance company's strategic goals is functioning effectively: Does it understand the overall risks it faces, compare this with its capital, and control its risks? This checklist was newly introduced. This checklist drastically added to and revised what was written in the Old Manual. Its revision reflects the content of the “Comprehensive Guidelines for Supervision of Insurance Companies” revisions (June 2009), referred to what is written about the Checklist for Comprehensive Risk Management of the Financial Inspection Manual, and considers the characteristics of insurance company operations.

Also, in the Old Manual, check items on financial soundness and actuarial matters,, such as appropriate accumulation of policy reserves, appropriate calculation of solvency margin ratio, business analysis and separate accounting, were placed in the “Checklist for Inspection of the Management System for Financial Soundness and Actuarial Matters.,” These are now positioned as subject to comprehensive risk management, and this checklist is rearranged into the “Checklist for Comprehensive Risk Management” (Attachment).

(6) Checklist for Insurance Underwriting Risk Management

Insurance underwriting risk refers to the risk that insurance companies may suffer losses due to changes in economic conditions and incidence rates of insured events,etc.,contrary to the forecasts made at the time of setting premium rates.This is a checklist to check whether the process of managing insurance underwriting risk is functioning effectively.

(7) Checklist for Asset Risk Management

Asset investment risk refers to the risk that an insurance company may incur losses due to fluctuations in value of assets and liabilities held. This is comprised of three risks: market risks, credit risks and real estate investment risks. This is a checklist to check whether there is an effectively functioning asset investment risk management system which matches the scale and nature of the insurance company's business.

Market risks and credit risks generally have large weights in asset investment risks borne by the insurance company. This is why these two risks are arranged as check items in an (Attachment) of the Revised Manual.

In asset investment, one must consider the liability characteristic of insurance companies, which bear obligations to pay insurance payouts over a long period when reasons occur for insurance payouts. The Old Manual has such check items written in consideration of this characteristic. The Revised Manual added new check items on whether in its asset investment, the insurance company holds sufficient assets with suitable characteristics such as maturity and liquidity, etc., to fulfill obligations in the future.

(8) Checklist for Operational Risk,etc. Management

Operational risk, etc.refers to “administrative risks,” “information system risk,” “liquidity risk” and “other operational risk” defined by the insurance company. This is a checklist to check whether management systems for each of these is functioning effectively.

In the Old Manual, among the “liquidity risk,” in the Checklist for Operational Risk, etc. Management, check items were created for “cash flow risk” (the risk of incurring losses due to being forced to sell assets at a price considerably lower than normal in order to maintain funds, owing to deteriorating cash flows as a result of: 1) decreasing insurance premium revenue as a result of a decline in new policy sales due to factors such as the deteriorating financial condition of the insurance company; 2) increased cash surrender benefit payments due to voluntary terminations of a large number of policies or large-lot policies; or 3) an outflow of funds in the aftermath of a large-scale disaster). In the Asset Investment Risk Management System Checklist, check items were created for “market liquidity risk” (the risk of incurring losses due to the inability to trade on a market or being forced to trade at a price considerably less advantageous than normal owing to a market disruption, etc.). In the Revised Manual, “cash flow risk” and “market liquidity risk” are closely related, so both are combined into “liquidity risk”, and its check items are created in the Checklist for Operational Risk, etc. Management.

5. Conclusion

The Insurance Inspection Manual is positioned as the handbook used when the inspector inspects an insurance company. Under the principle of self-responsibility, each insurance company is expected to refer to the Insurance Inspection Manual, fully utilize creativity and ingenuity, and develop a system in accordance with its scale and nature.

The FSA is informing its inspectors about the content of this revision, and continues working to “fully consider the scale and nature of the insurance company, while mechanical and uniform application” should be avoided.

Checkpoints, etc. of the Insurance Inspection Manual are shared with insurance companies, for enhanced dialogue between inspectors and insurance companies, as the FSA strives for more efficient and effective inspection operations.

* For details, please go to the FSA web site and access “ ‘Insurance Inspection Manual Revision (draft)’ - Measures taken after receipt of public comments” (February 4, 2011) from the Press Releases or Public Comments sections. (Available in Japanese only)

The Securities and Exchange Surveillance Commission (SESC), together with Local Finance Bureaus, has been conducting intensive inspections of investment advisories/agencies since March 2009, with focus placed on their legal compliance. On February 8, 2011, it summarized and published the results of the inspections. Furthermore, based on these, the SESC recommended the FSA Commissioner that it is necessary to introduce a personnel requirement for registration as an investment advisory/agency.

By publishing the results, the SESC intends to ask investment advisories/agencies to comply with the relevant laws and regulations, and to alert the public investors to be well aware of the issues identified, when signing investment advisory contracts with investment advisories/agencies.

I. Summary of Inspection Results

As of end January 2011, the SESC found legal violations in 47 of the 74 firms inspected and among the 74, serious legal violations were found in 11 firms. Accordingly, the SESC made recommendations to the FSA to take administrative disciplinary actions against them.

1. Main Problems

The main problems found in the inspections are as follows.

(1) Deviations from Investment Advisory/Agency Business

(i) Engagement in Unregistered Businesses (4 firms)

Two investment advisories/agencies were found to be engaged in solicitation and sales of unlisted stocks and one in solicitation of foreign investment securities, without the required registration of Type I Financial Instruments Business Operator. One firm was soliciting investment in collective investment schemes (investment partnerships) without the required registration of Type II Financial Instruments Business Operator.

These were effectively operating Type I and Type II financial instruments businesses without the required registration, thus evading the Financial Instruments and Exchange Act's regulations that aim at protecting the public investors under the registration system. Therefore, considering the severity and wrongfulness of the violations, the SESC made recommendations to take administrative disciplinary actions against all the four firms. One firm out of the four, in particular, was very malicious as it was engaged in the similar illegal activities identified through the past inspection that resulted in business suspension and improvement orders.

(ii) Name-lending to Unregistered Dealers (4 firms)

Two investment advisories/agencies were found to make arrangements for unregistered parties to engage in investment advisory business or sales of fund equities of a collective investment scheme under their names. One firm, though it did not lend its name, was found to have their own employees engage in sales of unlisted stocks and fund equities of an investment fund by an unregistered firm, while knowing that the latter did not have the necessary registration. Another firm outsourced fund management, while knowing that the outsourced party did not register as an investment management business.

In these cases, the registration system was evaded by allowing unregistered entities that are not subject to the regulations to operate regulated financial activities. Considering the severity and maliciousness of these illegal activities, recommendations were made to take administrative disciplinary actions against all the four firms.

(2) Inappropriate Operations of Investment Advisory/Agency Business

(i) Inappropriate Provision of Information to Customers (Advertisements with false information, documents to be provided prior to signing a contract were not provided, etc.) (33 firms)

Many firms were found to have provided their customers with very inappropriate information: e.g. items written in advertisements were deficient or false; solicitation materials with false displays were used to solicit signing of investment advisory contracts; and documents to be provided prior to, or upon, signing a contract were not provided or their contents were deficient.

Among these cases, the SESC made recommendations to the FSA to take administrative disciplinary actions against three firms that issued remarkably false advertisements or gave their customers no documents to be provided prior to signing a contract, considering the seriousness and maliciousness of these illegal activities.

(ii) Inappropriate Preparation and Management of Basic Books and Documents (Mandatory books were not prepared or stored, business reports with false contents were submitted, etc.) (16 firms)

The SESC found many legal violations with regards to basic documentation. For example, there were firms that did not make or store mandatory records of advices they have made to customers. Some firms were found to make false financial statements or submit business reports with wrong number of contracts and amount of investment advisory fees. Another firm filed a false report in response to an order from a Local Finance Bureau, aiming to conceal that it was soliciting investments in collective investment schemes without the required registration of Type II financial instruments business operator.

Among these, the SESC issued recommendations to the FSA to take administrative disciplinary actions against four firms that submitted misstated business reports aiming to conceal insolvency or that filed a false report in response to an order from a Local Finance Bureau, considering the seriousness and maliciousness of these illegal acts.

2. Causes of Legal Violations

Looking at the causes of these problems, in almost all cases, the officers of the investment advisories/agencies remarkably lacked basic legal knowledge and perception of the need for legal compliance. In these situations, it was found that the firms prioritized their own profits over compliance with laws and regulations.

II. Way Forward

1. Investment Advisories/Agencies

Investment advisories/agencies are strongly required to be aware of their duties for legal compliance as registered business operators and to comply with the laws and regulations to protect the public investors, with due regard for the above problems and causes.

In addition, the Japan Securities Investment Advisers Association, given the recent increase in its membership, is strongly expected to further demonstrate its role as a self-regulatory organization for thorough legal compliance of its members.

2. Securities and Exchange Surveillance Commission

(1) A Policy Recommendation

As described above, almost all cases of legal violations found in the inspections were caused by the remarkable lack of basic legal knowledge and recognition of the need for legal compliance among officers of the investment advisories/agencies inspected.

Considering these situations, under Article 21 of the Act for Establishment of the Financial Services Agency, the SESC made a policy recommendation to the FSA Commissioner on February 8, 2011 that, in order to further promote investor protection with regards to investment advisories/agencies, it is necessary to introduce a personnel requirement for registration as an investment advisory/agency, which will enable the FSA to refuse a registration application if the applicant is deemed to have inadequate officers to conduct investment advisory/agency business, such as those who lack relevant legal knowledge and recognition of the need for legal compliance. This personnel requirement has already been introduced for the other financial instruments business operators.

This is also expected, once introduced, to contribute to enhancing countermeasures to exclude organized crime from investment advisories/agencies business, while each government ministry/agency is supposed to work on these measures, following “Initiatives to Exclude Organized Crime from Company Activities” by the inter-ministerial Working Group on Comprehensive Countermeasures against Organized Crime, reported at the Ministerial Meeting on Measures Against Crime on December 14, 2010.

(2) Inspections

The SESC will continue inspections on investment advisories/agencies and when problems are found with respect to legal compliance, it will take strict actions such as making recommendations to the FSA to take appropriate administrative measures, seeking their correction and improvements.

* For more details, please visit Results of inspections of investment advisories/agencies (main points) (February 8, 2011)![]() on the SESC website. (Available in Japanese only)

on the SESC website. (Available in Japanese only)

Site Map

- Press Releases & Public Relations

- Press Releases

- Press Conferences

- Official Statements

- FSA Weekly Review & ACCESS FSA

- Speeches

- For Financial Users

- Others

- Archives

- Laws & Regulations

- Name of Laws and Regulations(PDF)

- Recent Changes (Legislation, Ordinances, Guidelines)

- Guidelines

- Financial Instruments and Exchange Act

- Financial Monitoring Policy

- Public Comment

- No-Action Letter System

- Procedures concerning Foreign Account Management Institutions